PISP – Payment Initiation

The solution that allows companies to accept payments via SEPA transfers, both standard and instant, and to easily integrate them into their collection applications or Ecommerce websites.

AIS and PIS solutions are not available in the UK. Fabrick provides these solutions only in Italy, Spain, France and Portugal. If your business has a registered office in Italy, Spain, France or Portugal and you would like more information, you can contact us here.

Frictionless payments integrated into the customer journey

Companies can offer their corporate and end-consumer customers the added opportunity to pay via account-to-account (A2A), i.e. directly from their current account, without interrupting the flow with the application they are in and without having to log on to their home banking.

Frictionless payments integrated into the customer journey

Companies can offer their corporate and end-consumer customers the added opportunity to pay via account-to-account (A2A), i.e. directly from their current account, without interrupting the flow with the application they are in and without having to log on to their home banking.

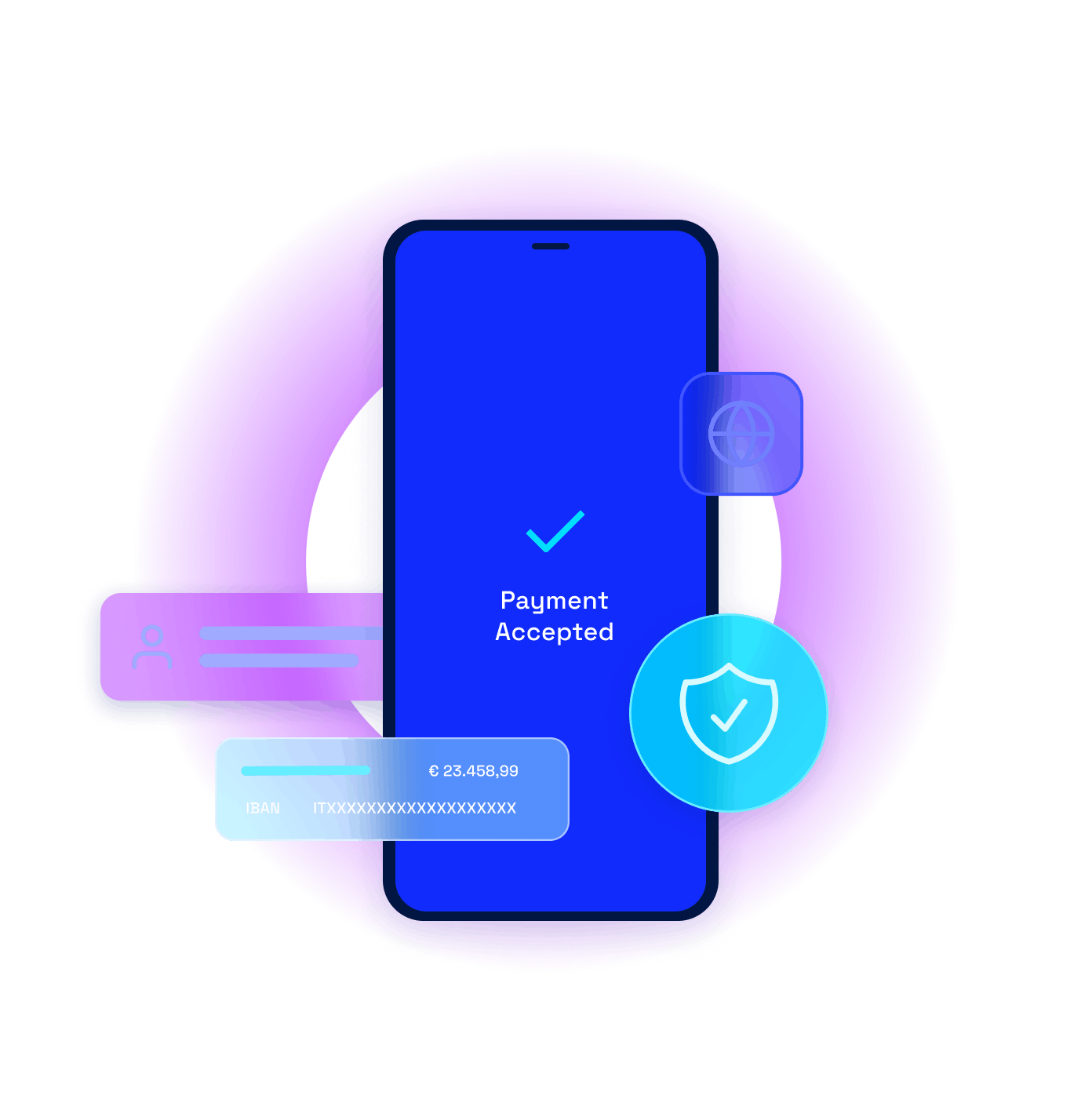

How A2A payments work

Fabrick provides its PISP licence and technology in 'as a service' mode, to facilitate all types of companies, including non-financial ones, to reap the benefits of Open Banking through an easily integrated solution.

In the initial payment phase (payment initiation), the end customer chooses the 'Payment from Account' service (payment initiation PIS or Account to Account A2A).

The user is directed to a Fabrick web page where they select their bank, accept the terms and conditions of service and the privacy policy.

The end customer authorises the transaction through Strong Customer Authentication (SCA), with a process similar to that used for online card purchases, then Fabrick sends the receipt and transmits the outcome of the payment to the company.

The credit transfer is credited in real time, in case of an instant SEPA credit transfer, or within two working days, in case of an ordinary SEPA credit transfer. In both instances, the credit transfer is irrevocable, guaranteeing the beneficiary the certainty of receipt of the funds.

The evolution of bank transfers

The fields required to make an A2A payment (amount, beneficiary and reference) are automatically pre-filled. This reduces the risk of errors during data entry and results in payments being pre-reconciled by default, which saves a great deal of work for the back office.

The application of a fixed fee per transaction reduces costs compared to traditional payment methods, especially for high value purchases. Moreover, as there are no intermediary networks between company and consumer, the payment is processed faster and once authorisation has been granted, it can no longer be withdrawn.

Use cases

Online stores can make pre-filled transfers from the customer's account.

This way merchants can save on commissions by offering an alternative payment method, ideal for large amounts and for those who do not dispose of credit or debit cards or do not want to use up their plafond.

Business customers are given access to tools to manage current accounts and cash flows automatically.

The service allows cash to be transferred among different company accounts, based on rules preset by the company itself. Balancing accounts based on expenses, optimising cash flows and moving balances when specific events occur are just a few practical examples.

Payments can be split amongst different company accounts, e.g. according to the balance available.

The operational and time-related costs of manual reconciliation processes are lowered, also due to the very nature of the service, which prevents any manual errors on the part of the customer when completing the online transfer.

The payment solution for remote collection without the need for an Ecommerce, simply by sending the customer a link via email or SMS (link that expires after a maximum of 90 days).

The link sent redirects the customer to a web page from which they can select their bank and authorise the payment, in order to immediately collect the goods or notify the company that they can arrange for shipment.

Latest Insights

The future of payments in 2024: international and consumer-focused

Cashless payments in the UK and worldwide

Digital payments and Mobility-as-a-Service (Maas)

Would you like more details about this product? Please fill out the form.

Contact our specialists to identify the most suitable solution for your needs.